ornstein_uhlenbeck, a Python code which approximates solutions of the Ornstein-Uhlenbeck stochastic differential equation (SDE) using the Euler method and the Euler-Maruyama method.

The Ornstein-Uhlenbeck stochastic differential equation has the form:

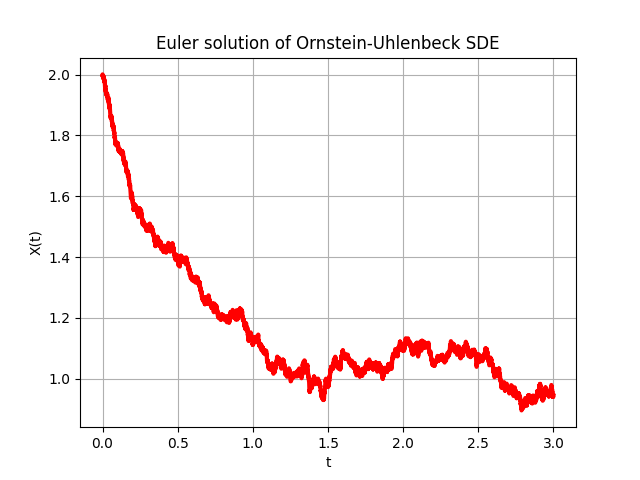

dx(t) = theta * ( mu - x(t) ) dt + sigma dW,

x(0) = x0.

where

The starting value x0 represents a deviation from the mean value mu. The decay rate theta determines how fast x(t) will move back towards its mean value. The coefficient sigma determines the relative magnitude of stochastic perturbations.

In general, the solution starts at x0 and over time moves towards the value mu, but experiences random "wobbles" whose size is determined by sigma. Increasing theta makes the solution move towards the mean faster.

The information on this web page is distributed under the MIT license.

ornstein_uhlenbeck is available in a C version and a C++ version and a Fortran90 version and a MATLAB version and an Octave version and a Python version.

black_scholes, a Python code which implements some simple approaches to the Black-Scholes option valuation theory, by Desmond Higham.

brownian_motion_simulation, a Python code which simulates Brownian motion in an M-dimensional region.

colored_noise, a Python code which generates samples of noise obeying a 1/f^alpha power law.

pink_noise, a Python code which computes a "pink noise" signal obeying a 1/f power law.

stochastic_diffusion, a Python code which implements several versions of a stochastic diffusivity coefficient.

{kind=link}

{kind=link}